The Market Balloons Over the Herd

The Market Balloons Over the Herd

Analysts Struggle to Explain Where The Market is Going

Despite the resilient strength of the job market, most indicators have rolled over. According to Clearbridge in Mar23, wherever you look is a sign of impeding recession.

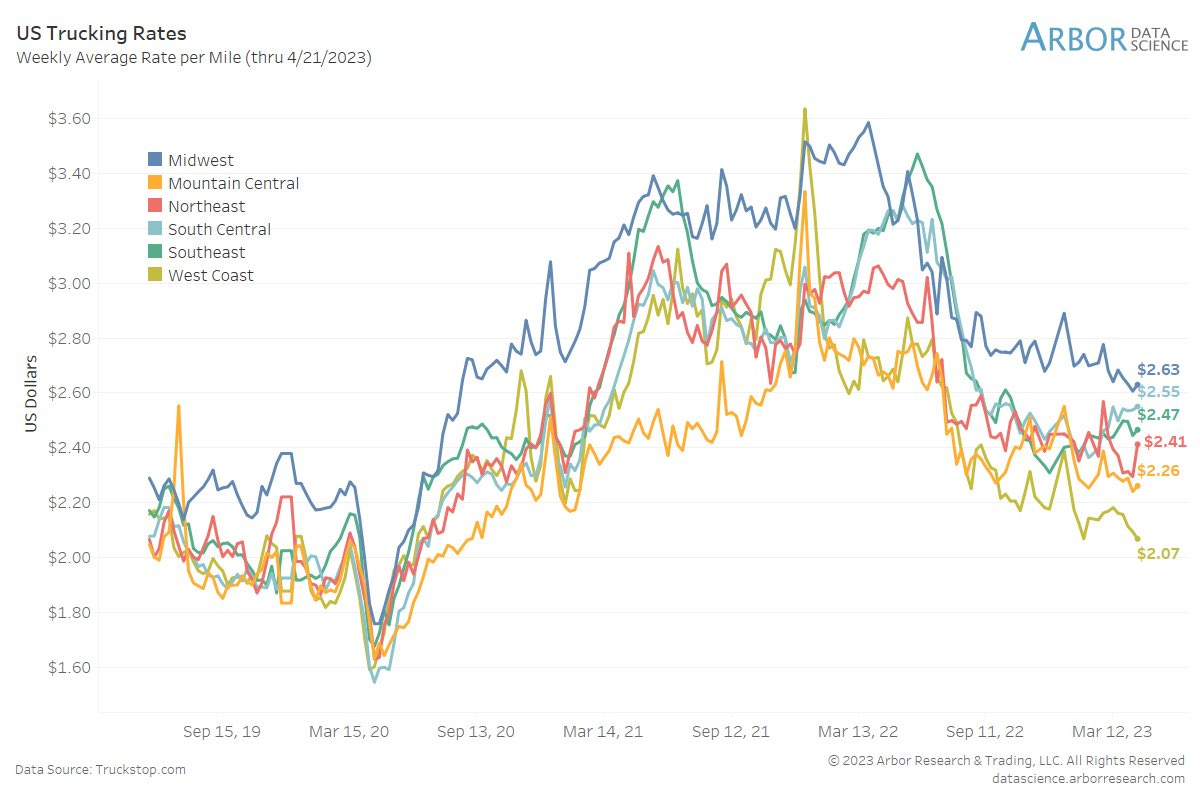

On the financial side, the yield curve is inverted, money supply works its way down from peak, and credit spreads are widening. Looking at business activity, profit margins are down and trucking rates are now moving sideways after falling sharply in the past year.

Now all eyes turn on the providential consumers. Are they ok? Well, not so well. Morale is still low, according to the latest UMich consumer index, as a consequence of more drastic financial conditions.

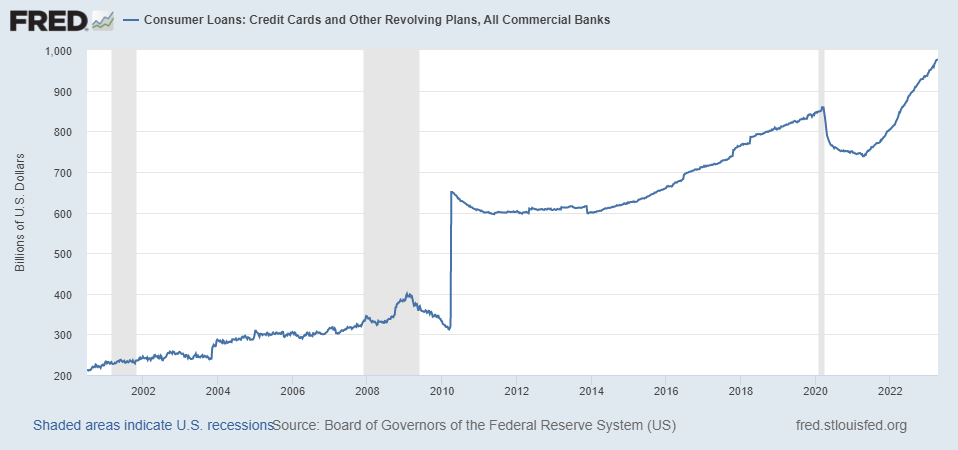

Personal spending is flat (literally 0% in Mar) even though outstanding credit card balances have been increasing savagely.

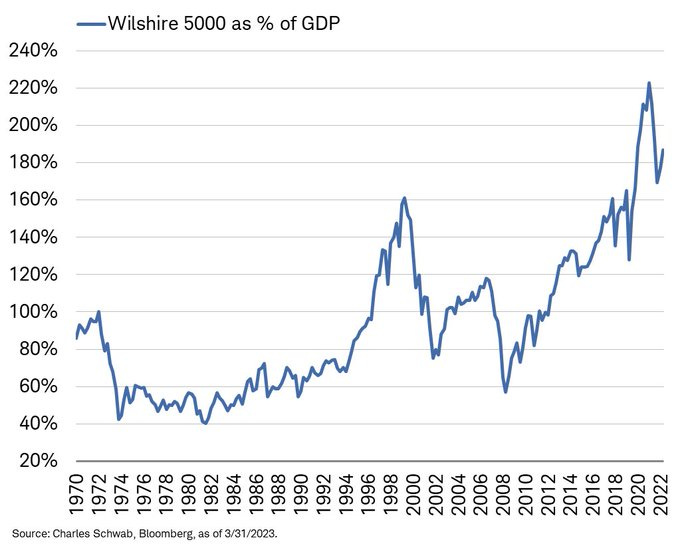

Yet, markets keep rebounding from the low point reached in October last year. S&P500 cranked up 8% so far this year, and PE stands at a toppish 19x, compared to MSCI World at 17x. The ratio of total US market capitalization over GDP, the so-called Buffet index, has come down from the hubris of 2022, but still stands at a staggering 160%.

To be fair, most the over-hype is due to the substantial leverage introduced by successive QE policies, which saw the Fed’s balance sheet inflate to $8TN. Nevertheless, the fairer indicator of Total market cap over (GDP+Fed’s balance sheet) still stands at a whopping 120%. The market is still pricing very optimistic forward expectations.

Is it due to massive technologic breakthrough, with the hopes of AI, EVs, and the likes? Maybe. There remains that this overvaluation is indicative of lower forward returns for investors.

So what to expect then?

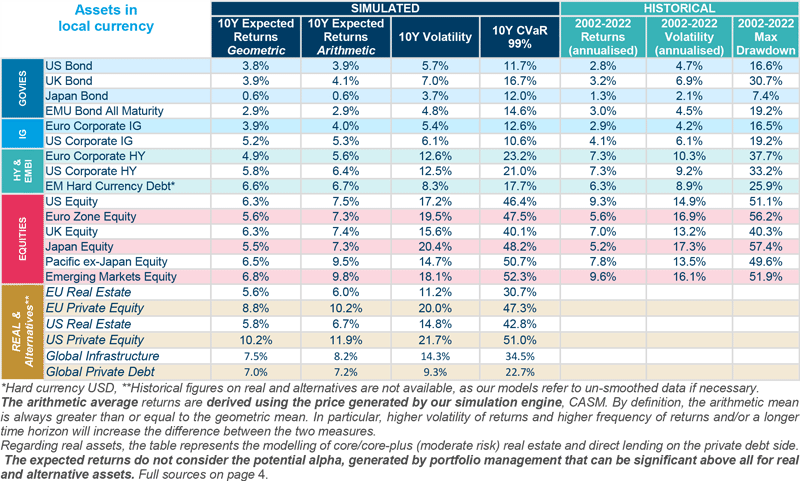

As modeled in 4Q22 by Amundi, an asset manager, the 10-year expected return of various asset classes rank between 0.6% and 10.2%, which probably sets the proverbial 60-40 portfolio in the 4%-to-5% area.

Let’s put it bluntly, there is very little incentive to take on risk when 10-year the risk-free rate is 3.45%. To put it another way, it calls for greater discernment. Typically, EM asset classes embed higher long-term returns if you can stomach the volatility. Private debt and private equity seem to be key areas of superior returns, as new vintage are reloading real estate credit deals at ~12% returns according to Blackstone.

The short-term market gyration will remain harder to predict though. A lot of macro parameters are on the move, with lower money supply, persistent inflation, and an increasing challenge to the USD, as the world currency. There are reasons to be cautious in this uncertain environment.

About –

360 Advisory LLC is a Boston-based RIA managing investments

👉Find Solutions 9–30am🐰🕳

Sources -

👉https://fred.stlouisfed.org/series/CCLACBW027SBOG#

👉https://research-center.amundi.com/article/asset-class-return-forecasts-q4-2022