Structurally Higher

Structurally Higher

A few forces are pushing for higher long-term rates and inflation

Let’s start with demographics. Ageing populations in Western countries and China has long been considered a long-term deflationary factor, based on a shrinking number of consumers. Sure, but in the meantime, boomers are coming to retirement with a large nest egg to spend, and our increased longevity is promising higher healthcare costs. We live longer, but also sicker as 40% of the US population is obese, causing all sorts of co-morbidity. Wegovy, the anti-obesity drug at a $16k clip annually, is more problem than solution to the burden of healthcare costs, notwithstanding that it doesn’t tackle the root causes: nutrition & exercise.

Secondly, US-China tensions are fanning the flames of reshoring, which is coming with an heftier made-in-America production cost, and a lesser benefit to importing Chinese deflation, as was the case since China accessed the WTO in 2001.

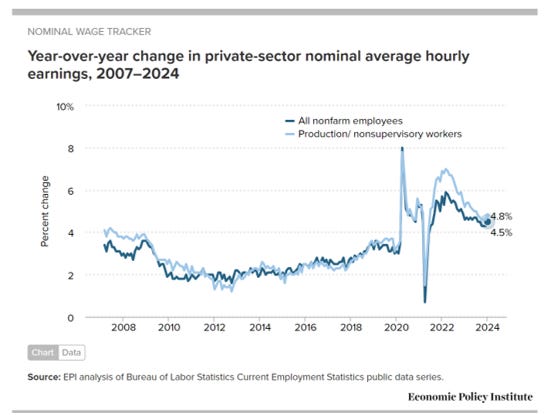

Thirdly, a growing social unrest is calling for a rebalancing of wages at the bottom end of the ladder. Average nominal wages, although increasing at 4.5% annually, are still meant to increase further to bring workers’ share of corporate income from 75% now back to 80% in 2010.

Lastly, the energy transition calls for an infrastructure build up. The IRA and its ~$400bn budget is the epitome of the investments needed to bring the grid up to par, and keep energy sources diversified.

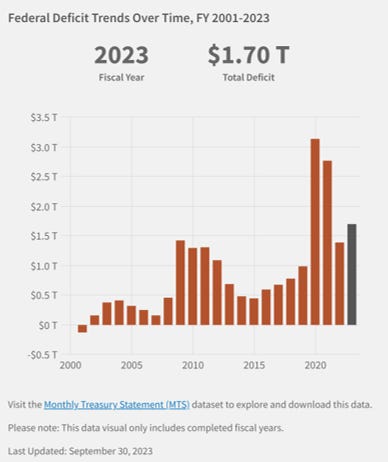

The result is already transpiring in structural deficits, not only in the US with $1,700 billion or 6% of GDP, but also in Europe. For example, France's public deficit for 2023 stood at 5.5% of GDP, or €154 billion, according to the national statistics institute INSEE.

To plug deficits, US debt could rise from 123% of GDP to 150% by 2030, and close to 200% by 2040. Such spending requirement would increase longer-term issuance, a supply shock, for which the Treasury would have to pay a higher premium.

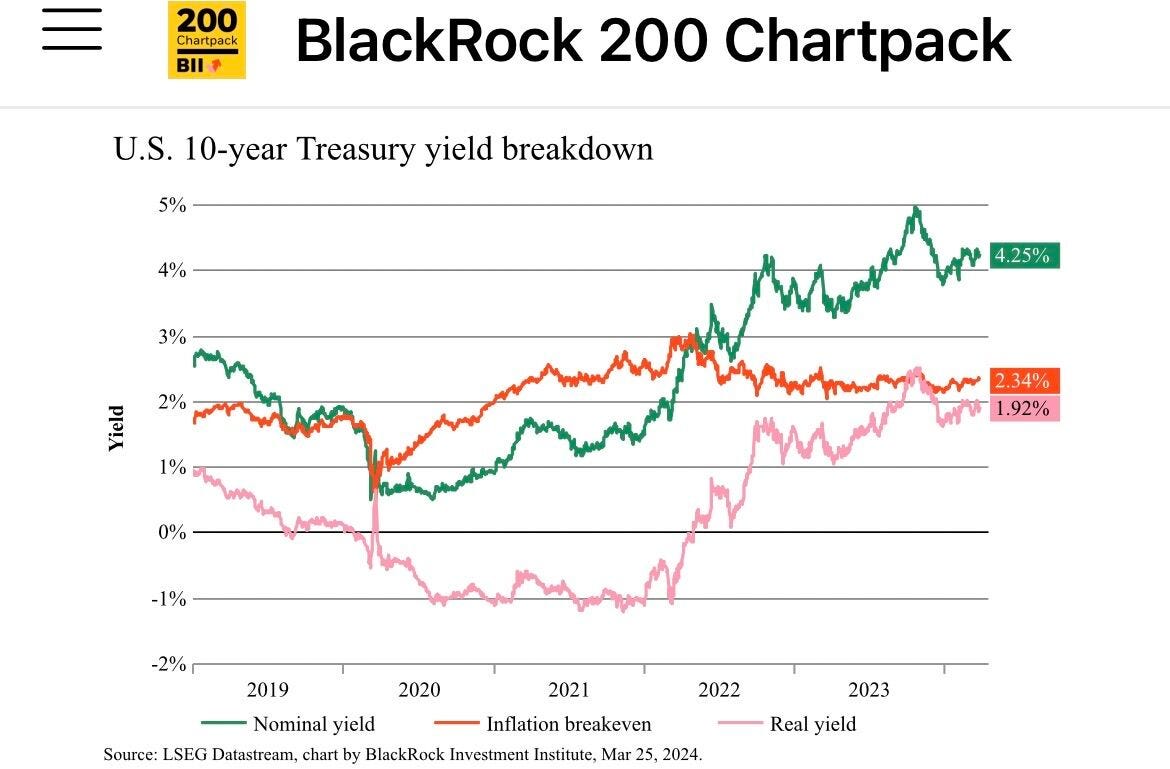

For now there is rather a "term discount" rather than a term premium, as curve is inverted and supply/demand action is mostly on the short end. But an increase of supply on the long-end would probably need to clear at a much higher rate.

Higher rates, and higher inflation could be a lasting feature of things to come.

As per Wei Li, strategist at Blackrock, “Long rates are drifting higher led by real rates. It’s not a problem for now - the narrative is still inflation falling, growth holding up, and cuts coming - until it is”.

For now, the soft landing scenario prevails, and the mood is risk-on. However, investors should be wary no to stack up too much of their money on long-term duration bonds, and should prefer the cushy 5-year belly of high-quality bonds instead.

Stay safe out there !

About –

360 Advisory LLC is a Boston-based RIA managing investments

👉Find Investment Solutions 9–30am🐰🕳

Sources -

Blackrock’s Larry Fink annual letter - Blackrock

Nominal wage - Economic Policy Institute

US deficits - US fiscal data