Buying the Dip?

Buying the Dip?

A sharp pull back in April raises a legitimate question

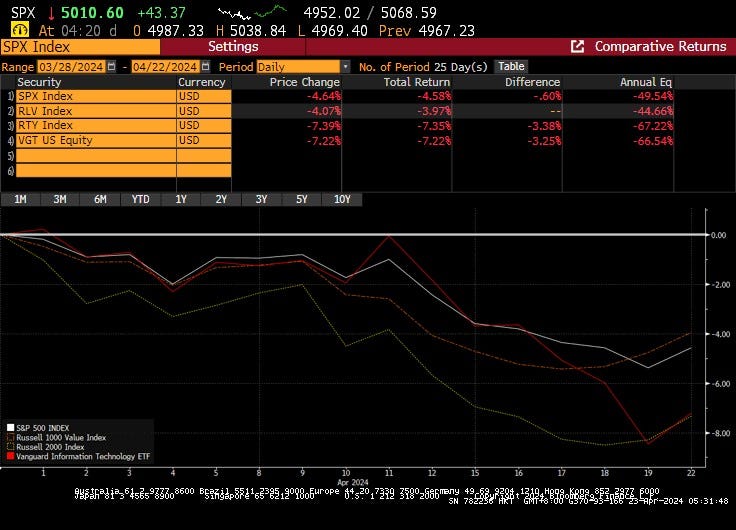

US stocks have slid between 4% and 7% since reaching peak at the end of March. Most affected by the risk-off are Tech stocks and Small caps. Investors are juggling with higher-for-longer rates and hopeful expectations for 1Q24 earnings.

Angst is gripping the market, as ASML pointed to a lackluster 2024 outlook, and TSMC cut down its growth forecast. Nvidia, the market’s AI darling, dropped 14% over the past week ahead of its results on 23Ap24.

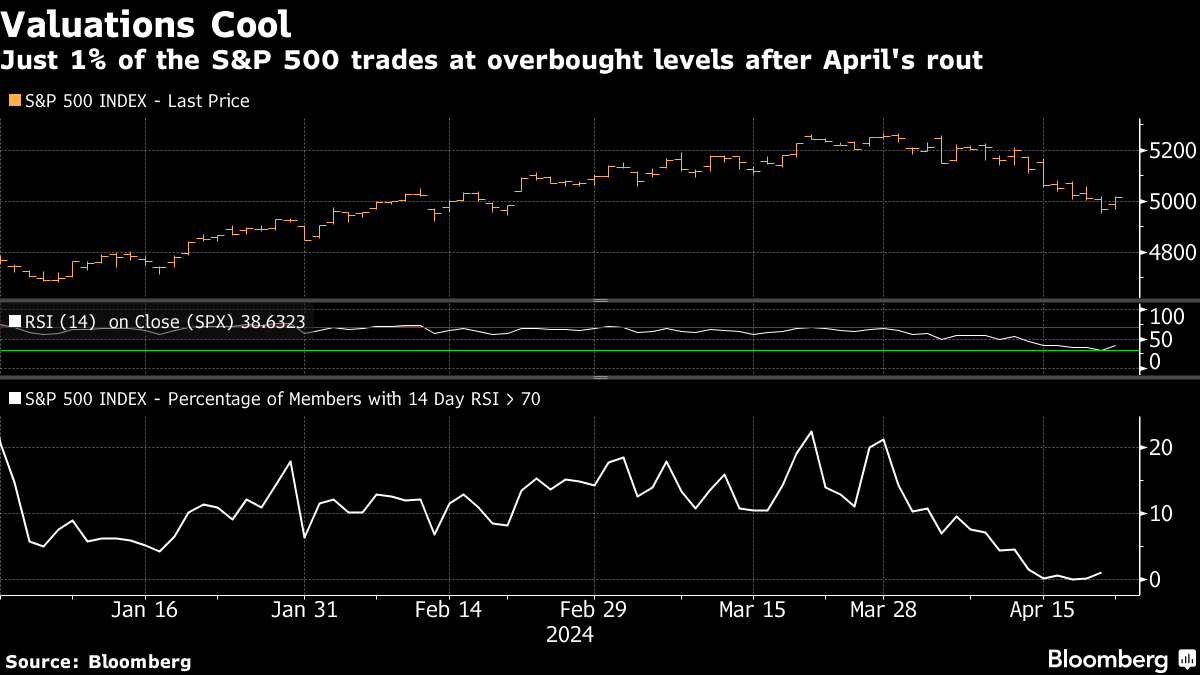

So, is it a good time to be greedy when others are fearful? According to Bloomberg, valuations cooled down since the sell-off and only 1% of the S&P500 is now into overbought territory, as defined by trading above their 14-day RSI (Relative Strength Index).

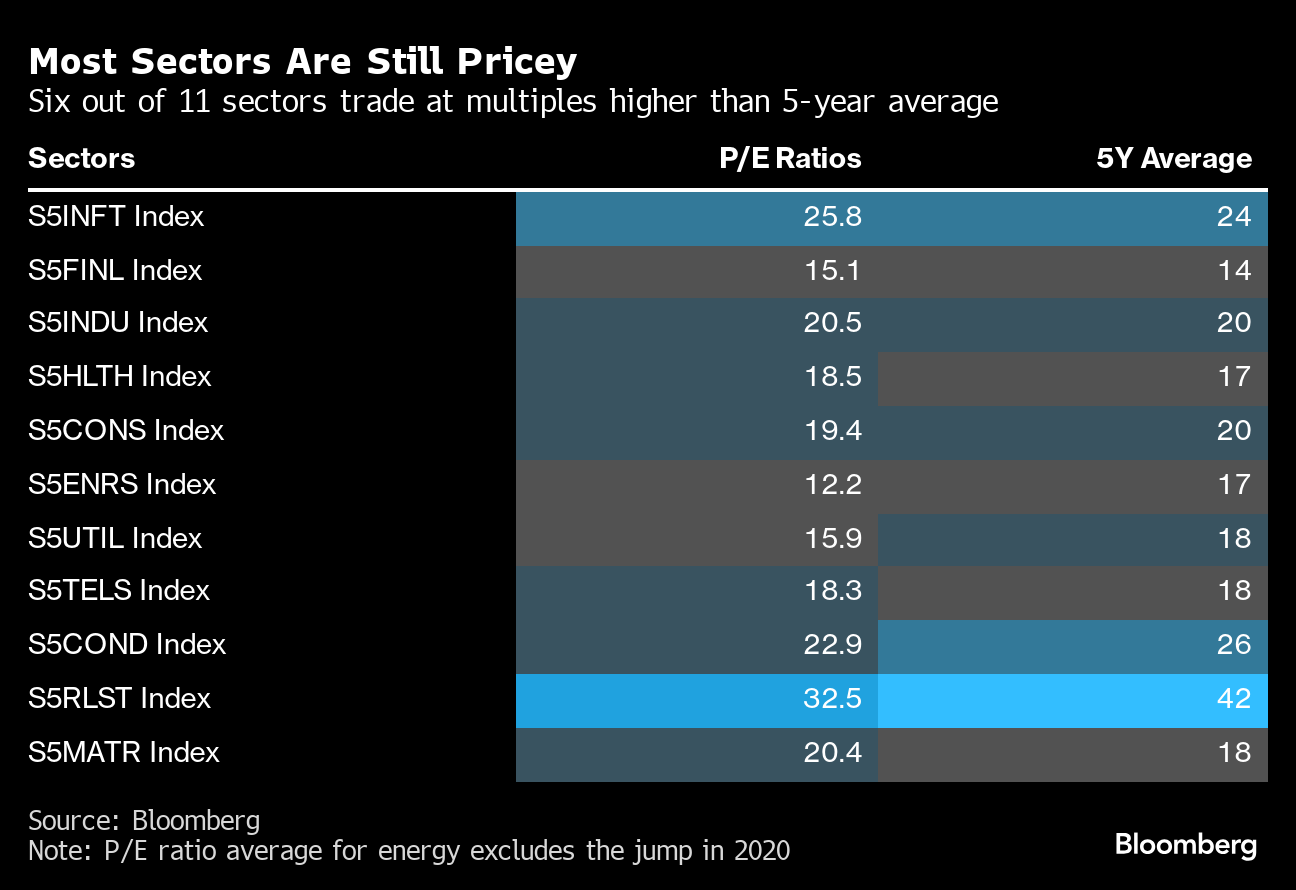

However, PE ratios still embed a great deal of forward growth. With the exceptions of Energy, Real Estate and Utilities, most sectors trade above their 5-year average PE ratios.

My view is that growth in 1Q24 kept surprising, and there is no reason it would not show in upbeat quarterly corporate results. As 159 of the S&P500 companies report earnings on the week of 22nd of April, I suppose we’ll find out pretty quickly.

There is no question that we’re surfing the peak of the valuation wave, but short of a brutal growth slowdown or a sharp uptick in inflation, there is little reason to panic just now. Equities, and large cap in particular, have been supported by astonishing earnings growth that still has momentum, until proven otherwise.

On fixed income, spreads have repriced slightly as well, and are back to early Feb24 level. Not a panacea, but better than a poke in the eye. On Govies, the 3-year at 4.8% looks decently attractive, and close to Oct23’s peak, even as the market still prices interest rate cuts this year.

That’s all for now !

About –

360 Advisory LLC is a Boston-based RIA managing investments

👉Find Investment Solutions 9–30am🐰🕳